Reading time: 2 minutes

Author: Thomas Masuch

Market research firms Wohlers Associates and Ampower reported growth of approximately 11 percent and 6 percent respectively in their latest annual reports. The reasons for this trend are highly complex. Key drivers included the Chinese AM market and the defense industry. Forecasts for the coming years are even more optimistic – a view that aligns with the results of the latest spring survey by the AM Working Group within the VDMA. Sales of desktop 3D printers are also experiencing tremendous growth, especially for use in industrial settings.

Overall market stable

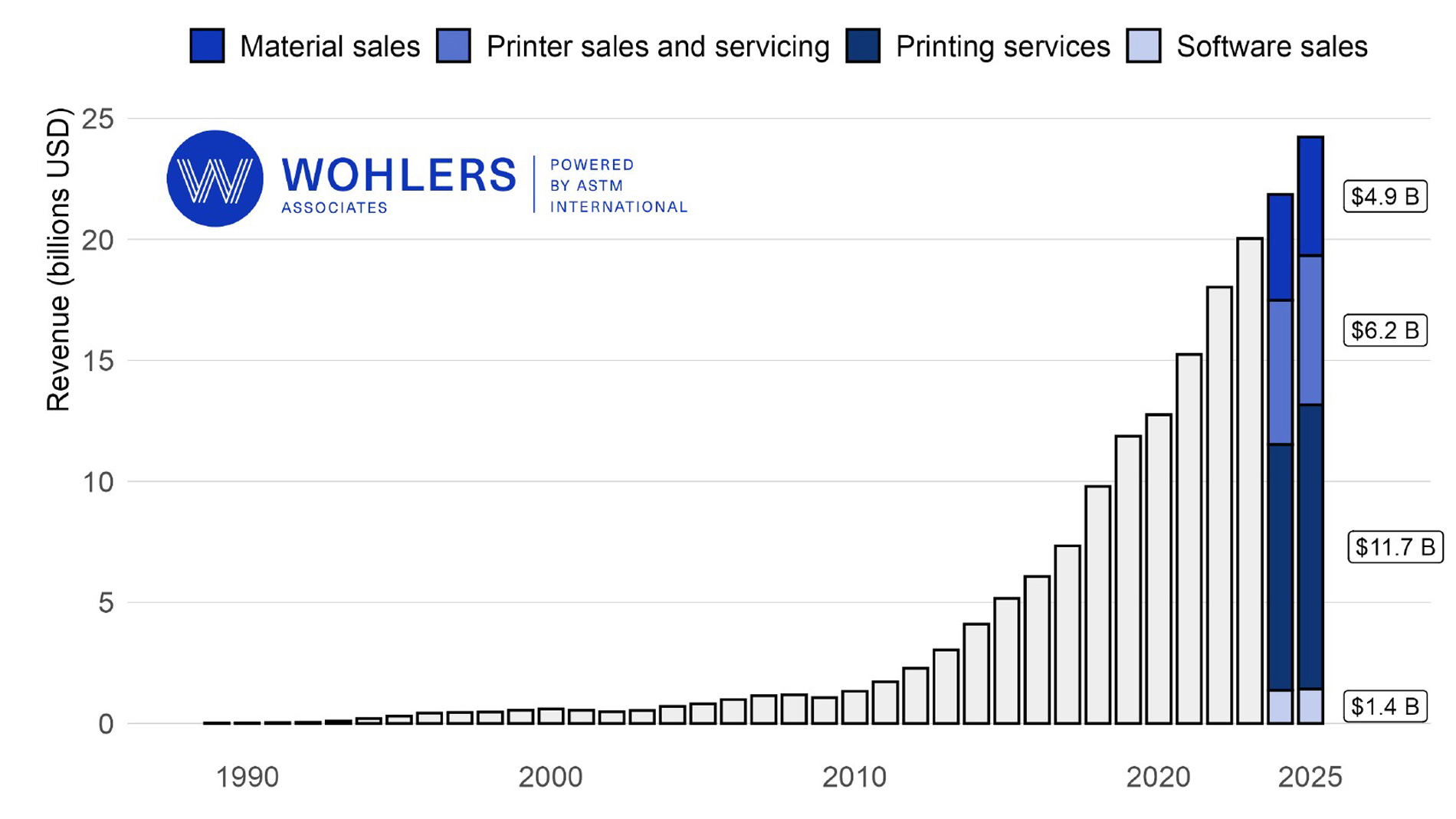

According to the Wohlers Report 2026, published by Wohlers Associates and powered by ASTM International, global AM revenues grew by 10.9% to approximately EUR 21 billion last year. The Hamburg-based experts at Ampower reported slightly lower growth of 6% to EUR 11 billion and forecast an annual growth rate (CAGR) of 14% for the next five years. “The main expected drivers are the increased demand for defense and aerospace programs, which are planned for the long term. Added to this is the breakthrough in the consumer sector (e.g., Zellerfeld, Apple). These markets were previously underrepresented and are now contributing to the increased growth expectations,” said Matthias Schmidt-Lehr, founder and CEO of Ampower.

Wohlers report: “Maturing industry”

Within the AM value chain, printing services showed the largest increase, up 15.5%, and now account for a 48% market share, according to Wohlers Associates. This is significantly higher than system sales and maintenance (26%), materials (20%), and software (6%). Wohlers Associates attributes the relatively modest 3.6% growth in AM system revenue to the fact that, in this “maturing industry,” existing systems are being utilized more efficiently, while value creation is increasingly concentrated on production and services.

The Wohlers Report 2026 also highlights sharply diverged regional trends, with companies in the Asia-Pacific region reporting average revenue growth of 19.8%, compared with 12.6% in the Americas and 9.0% in Europe, the Middle East, and Africa. Mahdi Jamshid, Director of Market Intelligence at Wohlers Associates, sums up: “Growth continues, but it is more uneven, more regional, and more closely tied to real production outcomes.”

Ampower: Defense and consumer goods drive the market

According to the Ampower Report 2026, one of the key drivers of the global AM market was the defense industry, which has grown significantly in recent years and is increasingly turning to AM as a production method: “Around the world, armed forces are using AM to solve challenges in the supply chain and spare parts procurement, while military OEMs and startups are utilizing the technology for the latest missiles, hypersonic missiles, spare parts for ship castings, and drones.”

Technologically, PBF remains the top-selling AM technology in the metal sector, generating equipment sales of more than EUR one billion. According to Ampower, this corresponds to a market share of over 80%. It is therefore not surprising that a growing number of suppliers are entering the market: In 2025, the number of PBF equipment manufacturers rose again, from 96 in 2024 to 107. An increase in new market entrants was particularly evident in China. At the same time, the top 10 PBF OEMs account for 78% of revenue in this sector. That is a significant figure, though slightly less than the 80% recorded in 2024. The top 10 companies include, for example, EOS, Nikon SLM Solutions, Colibrium Additive, as well as Chinese OEMs such as BLT and Farsoon.

![Global metal and polymer Additive Manufacturing market 2020 to 2025 and forecast 2030 [in EUR billion]. Image: Ampower](/content/dam/messefrankfurt-mesago/formnext/2026/images/formnext_mag/1900x1069/Ampower-market-growth.jpg)

Desktop printers generate sales on a par with industrial systems

In its report, Ampower analyzed desktop polymer printers priced under EUR 10,000 for the first time: This segment has recently seen growth of over 30%, while sales of industrial systems rose by 6 to 8% year-over-year. “The desktop segment is becoming increasingly important. The conventional distinction between ‘consumer’ and ‘prosumer’ no longer applies.” As a result, revenue from desktop printers has nearly caught up to the combined level of industrial metal and polymer AM systems. One example of this tremendous growth is Bambulab, which forecasts revenue of over EUR 1 billion.

VDMA outlook: Cautious in the short term, optimistic in the medium term

Positive momentum in the AM industry is also evident from the VDMA’s 2026 spring survey: “After a period of disillusionment, the Additive Manufacturing industry is noticeably stabilizing,” said Dr. Markus Heering, Managing Director of the Additive Manufacturing Working Group (AG AM) at the VDMA. Accordingly, companies have significantly more positive expectations for the coming two years.

The business situation for AG AM member companies within the VDMA has improved slightly compared to fall 2025: The number of companies reporting declining sales continues to fall (currently 19 percent), while 49 percent of companies report positive business development. In particular, companies anticipate a noticeable upturn in the medium term.

At the same time, international competitive pressure continues to intensify. 52 percent of companies view Chinese suppliers as competitors, which represents a clear increase compared to previous surveys. On the other hand, the share of companies that consider German competitors to be particularly relevant has dropped from 67 to 59 percent.

The survey results also reveal the growing importance of additive series production. For the first time, companies reported that series products account for the largest share of additively manufactured components.